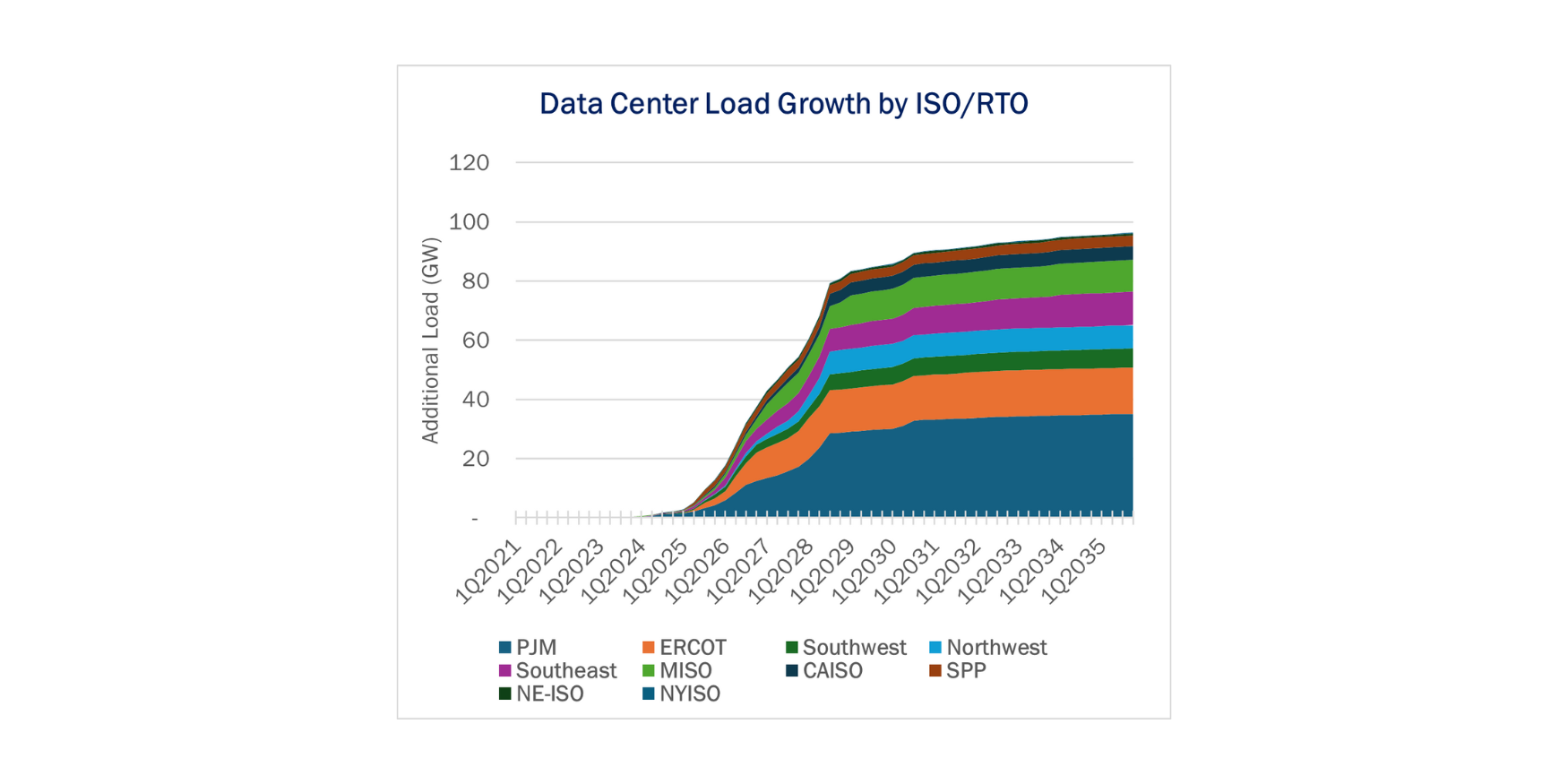

Executive Summary:

Infrastructure: Permian gas is entering a more tempered growth phase as producers respond to lower oil prices and shifting economic priorities.

Rigs: The US rig count decreased by 7 for the June 07 week to 521.

Flows: US natural gas pipeline samples averaged 69.5 Bcf/d for the week ending June 15, down 0.4% W-o-W.

Storage: The EIA reported a 95 Bcf injection for the week ending June 13, 1 Bcf lower than consensus estimates.

Infrastructure:

After years of aggressive development, the Permian Basin is entering a more tempered growth phase as producers recalibrate activity in response to lower oil prices and shifting priorities.

Diamondback Energy (FANG) set the tone last quarter, trimming its 2025 capital budget by $400MM and unveiling plans to drop 3 rigs and a frac crew from the Permian in 2Q25. Management made it clear: growth is viable at $60/bbl WTI, but anything below that price level puts the basin in maintenance mode — with potential for activity to stall around $50 WTI.

Despite natural gas accounting for over 20% of total production (as measured on a boe basis), FANG reported that gas sales make up less than 1% of total revenue from customer contracts. This does not translate into strong growth prospects for gas-directed development.

In terms of gas pipeline infrastructure, current Permian gas production already exceeds total effective egress capacity, leading to an estimated flaring balance of nearly 0.5 Bcf/d in 2025 in East Daley’s latest Permian Supply & Demand model. While this highlights the urgency for additional takeaway, a potential overcorrection looms.

We expect ~4.5 Bcf/d of new pipeline capacity to come online by early 2027, aimed at connecting Permian supply to Gulf Coast demand centers. However, based on the lower WTI forward strip, East Daley does not forecast enough gas production growth to fill this capacity. This estimate does not include the recently proposed 2.4 Bcf/d Tallgrass Permian-to-REX connector.

To utilize this additional takeaway by 2030, the basin would require ~60 active rigs in the gassier windows beginning in 2026 — an impossible scenario under current market conditions stressing capital discipline. This sets up a near- to medium-term period of underutilized infrastructure and constrained economics for some midstream assets.

Looking ahead, market forces may provide relief. Oil prices have rebounded sharply in the last week after Israel launched missiles at Iran targeting the country’s nuclear program. It remains to be seen whether the gains will hold in crude, or if Permian producers chase higher prices with increased drilling.

On the gas side, East Daley expects Waha basis to strengthen starting in 2027, driven by increasing Gulf Coast LNG demand. Although the anticipated price uplift may not be sufficient to prompt more gas-directed drilling, it could help producers recover sunk costs on firm transport agreements and improve profitability.

Rigs:

The US rig count decreased by 7 for the June 07 week, standing at 521. The Permian (-3), Bakken (-2), Anadarko (-1) and Powder River (-1) lost rigs while the other basins remained flat W-o-W.

On the midstream side, Enterprise Products (EPD) is down 2 rigs net with losses on its Permian and Eagle Ford systems. Phillips 66 (PSX) is up 3 rigs total with wins on its Permian systems.

See East Daley’s weekly Rig Activity Tracker for more information.

Flows:

US natural gas volumes averaged 69.5 Bcf/d in pipeline samples for the week ending June 15, down 0.4% W-o-W from 69.8 Bcf/d the previous week.

Gas-driven basins declined 0.4% W-o-W to average 44.1 Bcf/d. The Haynesville sample declined 2.9% to 10.6 Bcf/d. The Marcellus+Utica gained 0.2% to 32.8 Bcf/d.

Liquids-driven basins decreased 0.3% to 18.0 Bcf/d. The Eagle Ford sample held flat while Permian gas declined 0.5% to 5.8 Bcf/d.

Storage:

The Energy Information Administration (EIA) on Wednesday reported a 95 Bcf injection for the week ending June 13, 1 Bcf lower than consensus estimates. EIA released the storage survey a day early due to the Juneteenth holiday Thursday.

The 95 Bcf report broke a string of seven consecutive 100+ Bcf weekly injections. Nevertheless, the 95 Bcf injection was still significant for the second full week of June and pushed the surplus to the 5-year average up by 23 Bcf to 162 Bcf. The storage deficit vs last year fell by 23 Bcf to 231 Bcf. Storage currently totals 2,802 Bcf.

Cash prices remain relatively weak below $2.70/MMBtu while the prompt-month July Henry Hub contract is more than $1.00 higher. This wide of a spread between cash and prompt is pretty unusual. Speculators are betting on strong demand for the balance of June and for July, while cash prices reflect that this demand hasn’t shown up in reality. The June 22-28 week will be interesting to see how far the July contract retreats before bidweek begins. Next week will also be the hottest of the summer to date, which will likely spark a ‘buy the rumor, sell the news’ scenario for many traders rushing out of long positions.

Calendar:

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

-1.png)