Executive Summary:

Infrastructure: PAA adds $3B in dry powder for further M&A after $3.75B NGL asset sale.

Rigs: The total US rig count decreased during the week of June 8 to 524.

Storage: East Daley expects a 638 Mbbl withdrawal into storage for the week ending June 20.

Rigs: The total US rig count decreased during the week of June 8 to 524. Liquids-driven basins decreased by 5 W-o-W from 415 to 410.

- Permian (-3):

-

- Midland (-2): Diamondback Energy, Rockport Energy Solutions

-

- Delaware (-1): Mewbourne Energy

- Anadarko (-2): Pickrell Drilling, Double G Petro

- Powder River (-1): 1876 Resources

- Eagle Ford (+1): CML Exploration

Infrastructure:

Plains All American (PAA) will inject ~$3.0B of net proceeds into its war chest following the sale of its Canadian NGL assets to Keyera (KEY.TO) for $3.75B (C$5.15B). The transaction announced June 17 is slated to close in early 2026, and the Canadian NGL assets will be classified as discontinued operations as of June 30, 2025. The divestiture streamlines PAA’s asset footprint to focus on crude oil infrastructure.

East Daley Analytics’ PAA Financial Blueprint details the company’s results. Plains delivered 1Q25 Adj. EBITDA of $754MM and exited the quarter with $427MM of cash vs $8.2B of long-term debt. PAA’s leverage ratio of 3.3x is at the low end of its 3.25x–3.75x target. The disciplined credit profile underpins Plains’ capacity to deploy capital without threatening its covenant headroom.

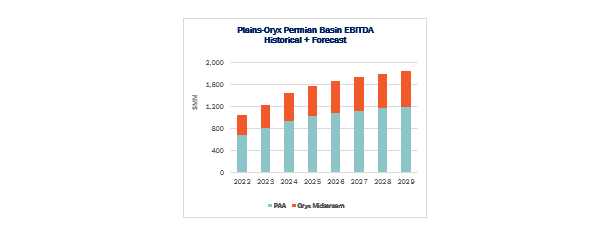

One potential use of the Keyera proceeds is to consolidate its Permian Basin joint venture with Oryx Midstream. On a consolidated basis, Plains Oryx Permian Basin FY24 Adj. EBITDA was ~$1.45B, 65% (~$940MM) attributable to PAA and 35% (~$506MM) to Oryx.

Recent bolt-on transactions have traded at multiples ranging from 6.3x (ONEOK’s (OKE) Medallion gathering acquisition) to 9.5x (Sunoco’s (SUN) acquisition of NuStar Energy LP). Applying a mid-cycle 7x EBITDA multiple to the JV implies an enterprise value of ~$10.15B, so a 35% interest would cost ~$3.6B – likely within PAA’s allocation of capital.

With sub-3.5x leverage, ~$3B of firepower and clear historical EBITDA multiples, PAA is well positioned to execute a near-term, accretive purchase of the remaining 35% JV stake. Such a move would simplify governance, capture full cash-flow upside, and reinforce PAA’s disciplined M&A and value-creation thesis.

PAA could also target sizeable crude oil infrastructure disposals by its peers. Kinder Morgan’s (KMI) Products Pipelines & Terminals segment includes condensate processing, crude gathering pipelines and related terminals that are largely ancillary to its natural gas transmission business. Phillips 66’s (PSX) FERC-regulated crude oil and products pipelines generated ~$518MM of Adj. EBITDA. These non-core assets represent acquisition opportunities that dovetail with PAA’s disciplined growth thesis.

Storage

East Daley expects a 638 Mbbl withdrawal into commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending June 20. We expect total US stocks, including the SPR, will close at 819.5 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.13% W-o-W across all liquids-focused basins. Samples decreased 6.44% in the Gulf of Mexico and 1.35% in the Eagle Ford. However, these gains were partially offset by a 0.81% increase in the Williston. The Rockies and Gulf of Mexico have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

We expect US crude production to be 13.43 MMb/d. According to US bill of lading data, US crude imports decreased to 5.5 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Nigeria.

As of June 20, there was ~55 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to increase to 17.14 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 21 vessels loaded for the week ending June 20 and 26 the prior week. EDA expects US exports to be 3.36 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered to Choctaw February–May ‘25 and 2.4 MMbbl to be delivered to Bryan Mound April–May ‘25. The SPR has 399.8 MMbbl in storage as of June 20, 2025.

Regulatory and Tariffs:

Presented by ARBO

Bridger Pipeline, LLC Rates were increased by the FERC index. Joint rates are less than or equal to the sum of the local rates. Effective July 1, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)